Portfolio Manager Insights | Weekly Investor Commentary - 9.1.21

Click here for the full commentary.

A common adage in boxing is to watch your opponent’s shoulders and not their hands. Focusing on where the motion of a punch begins, rather than where it ends, allows you to react appropriately and accurately. The same is true when investing – it’s better to focus on the economy and long-term trends that drive markets and policy, rather than solely on outcomes such as Fed decisions and past returns. In other words, the best way for investors to position their portfolios today is to better understand where we are in the business and market cycles.

The path to normal monetary policy by the Fed and other central banks is a long one. During the last cycle, the Fed officially announced plans to taper its asset purchases at the end of 2013, began raising rates at the end of 2015, and did so until the second half of 2019. The Fed was just as measured in its approach after the dot-com bust when it raised rates slowly but steadily across 17 consecutive meetings from 2004 to 2007. The onset of tapering, and even the first rate hike in a cycle, is just the first step.

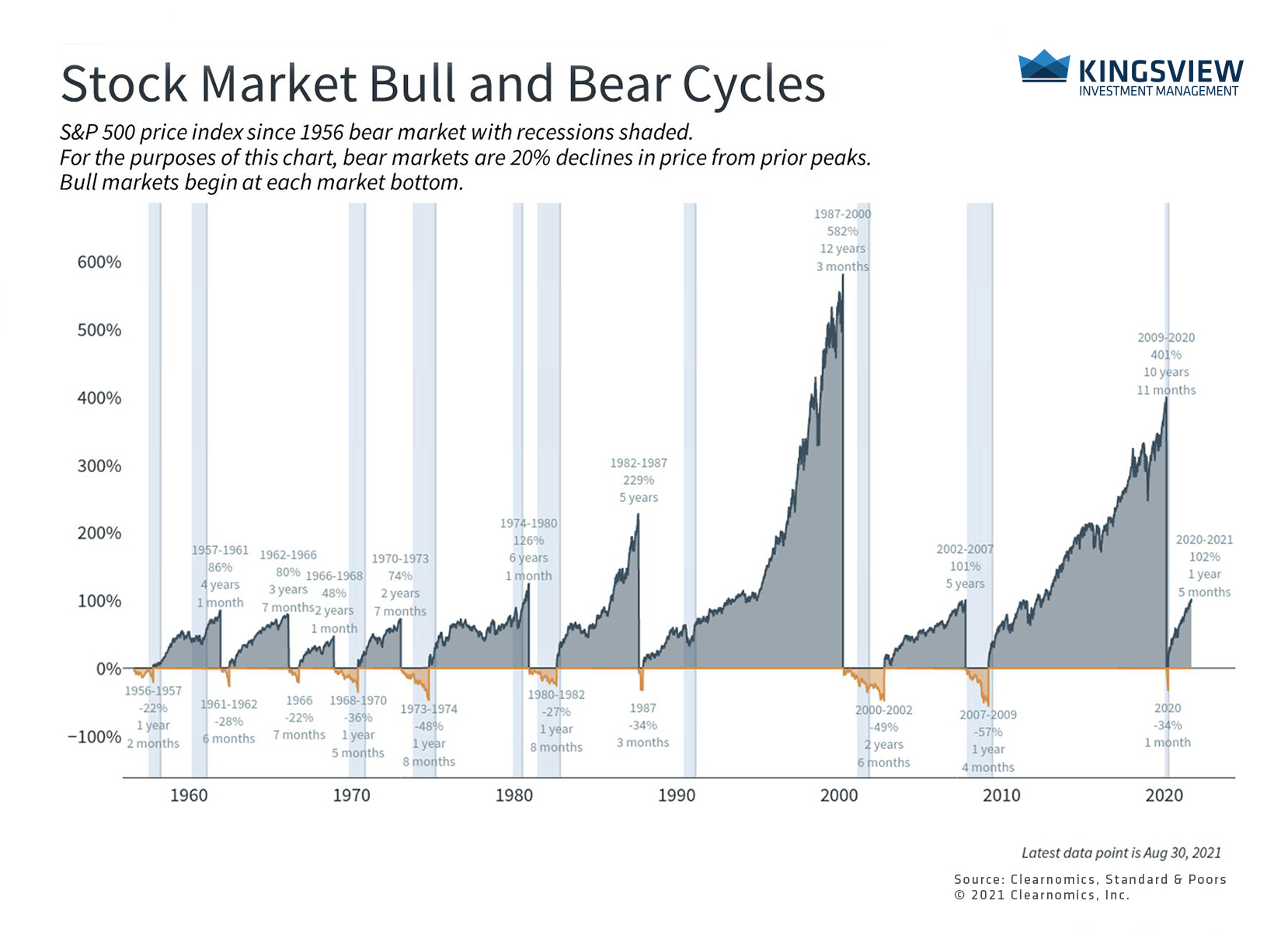

It is still early in the bull market and expansion

KEY TAKEAWAYS:

KEY TAKEAWAYS:

- The average market cycle has lasted between 5 and 12 years over the past 40 years.

- Although the recovery has been swift, growth trends suggest that the market cycle can still go a long way.

Today, market participants widely expect a change in policy, especially after Fed Chair Powell’s recent Jackson Hole speech. This is because economic conditions are favorable and although the pace of growth may slow a bit, the expansion is still robust. As a result, corporate profits are accelerating further. Consensus estimates are for S&P 500 earnings-per-share to reach almost $198 in 2021. This would represent a staggering 46% annual growth rate and help to support markets by bringing valuation levels back down to earth.

In broader terms, investors are accustomed to distinguishing between cyclical and “secular” (financial industry jargon for “long-term”) trends. Cyclical trends are those related to the natural ups and downs of the business cycle, such as those stocks and sectors that benefit from initial recoveries versus the later stages of an expansion. Secular trends are those that cut across cycles, such as trends in technology and global trade.

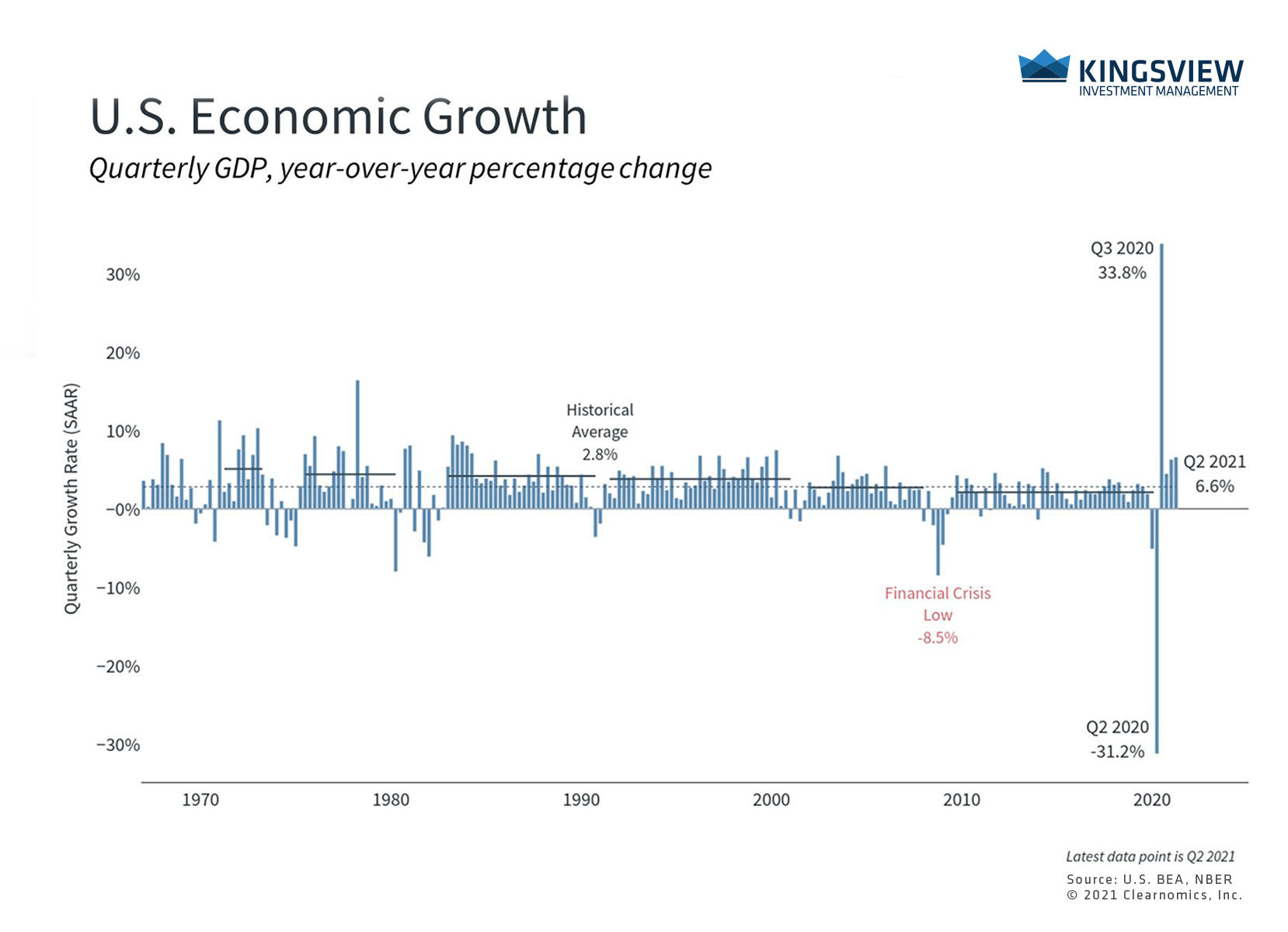

Economic growth is expected to be strong

KEY TAKEAWAYS:

- Last week’s upward revision to Q2 GDP showed that the economy grew by 6.6% during that quarter.

- The economy is expected to grow at a robust pace before it inevitably decelerates to more historically normal levels.

What’s made this distinction challenging has been the sharp initial recovery that boosted inflation and growth measures well beyond recent norms. There is a great deal of debate over whether these data are a result of cyclical or secular trends. The best answer today seems to be neither: these may simply be one-time events due to the nature of the crisis and rebound. While some effects, such as supply and demand disruptions in semiconductors or building materials, may linger for months, this is different from arguing that there are cyclical forces that will boost inflation for years to come.

In the end, it’s important for long-term investors to remember that crises are swift and abrupt while expansions are slow and steady. The National Bureau of Economic Research has officially declared that the COVID-19 recession lasted only 2 months. The markets bottomed out over the course of one month and recovered about 5 months later. In contrast, this bull market has now lasted almost a year and a half, and bull markets since the 1980s have lasted between 5 and 12 years.

Valuations are not cheap but may come down over time

KEY TAKEAWAY:

- Valuations across the broad market have been high due to the fast market recovery. However, strong and accelerating earnings are helping to deflate these lofty valuations.

It’s natural for investors to want to know exactly what’s around the bend, and to react to every event. But like the boxer who bobs and weaves too much in response to their opponent’s gloves, investors may only tire themselves out. Focusing on the underlying economic trends helps investors avoid having a short-sighted view of their portfolios. Investors should focus on the overall business cycle and long-term trends rather than day-to-day events.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2021)