Portfolio Manager Insights | Weekly Investor Commentary - 7.28.21

Click here for the full commentary.

As the economy shifts from recovery to expansion, one challenge for investors continues to be the high level of valuations. In the long run, valuations are investors’ best North Star since they don’t just tell us how much something costs, but also what we get for our money. They are correlated with portfolio returns for this reason – i.e., buying when the market is cheap improves the odds of success, and vice versa. After a spectacular recovery, what can investors expect in the years to come?

The most important thing for investors to remember is that valuations are a much better indicator of whether investments are attractive than prices alone. Prices can rise over long periods of time, just as they have for the U.S. stock market over the past century, despite bear markets and short-term corrections. Comparing prices today to previous peaks and troughs doesn’t consider differences between these time periods. Valuations, on the other hand, “normalize” prices by some important measure such as sales, earnings or cash flow. This adjustment makes prices more comparable over time to determine whether an asset class, sector or individual investment is attractive.

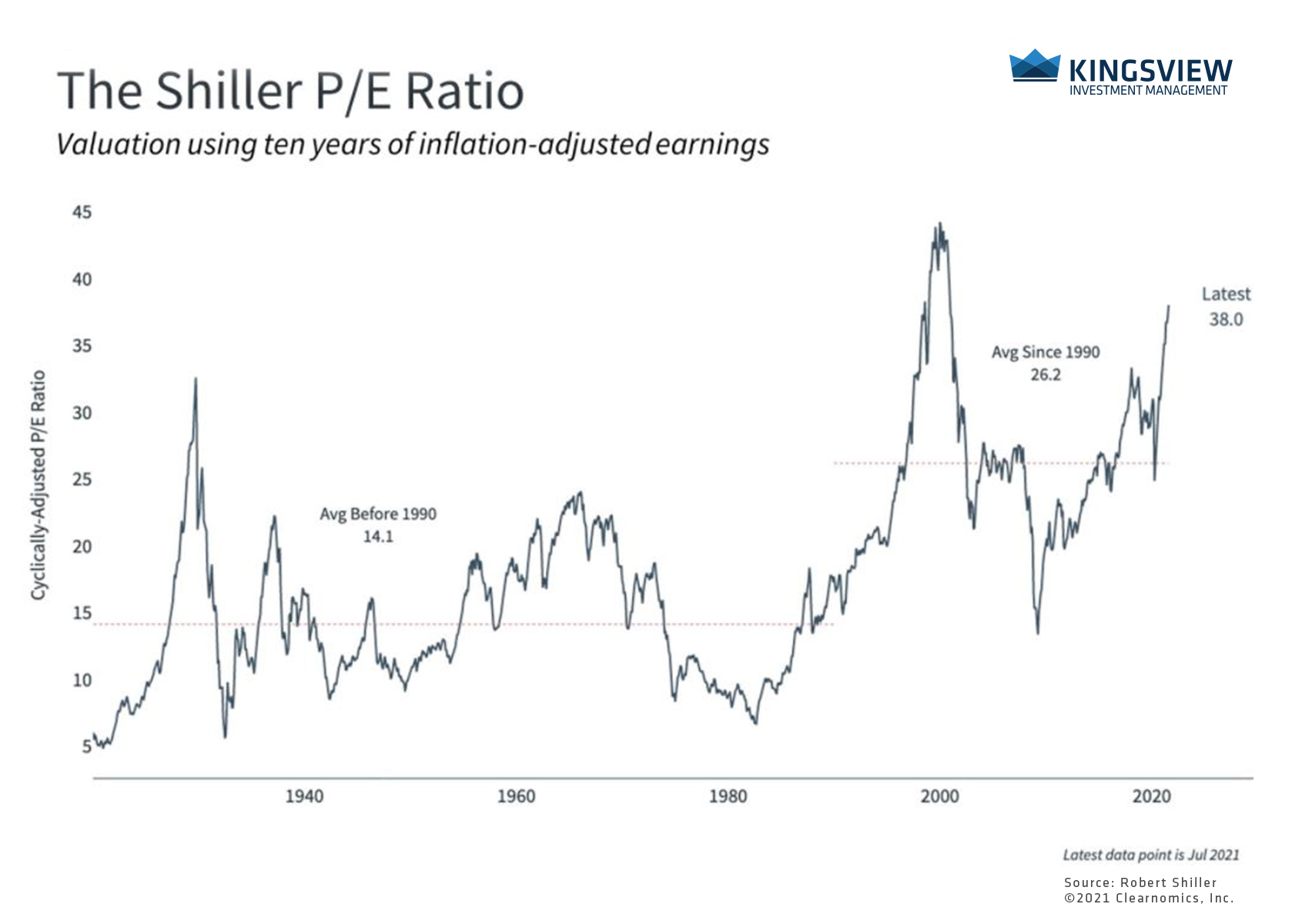

Long-run valuations are near historic peaks

KEY TAKEAWAYS:

KEY TAKEAWAYS:

- Measures such as the Shiller P/E ratio, which uses ten years of inflation-adjusted earnings in the denominator, are near historic levels. This and similar valuation measures are correlated with long-run portfolio returns.

- However, it’s possible for these measures to improve (i.e. decline) as earnings and other fundamentals catch up to prices.

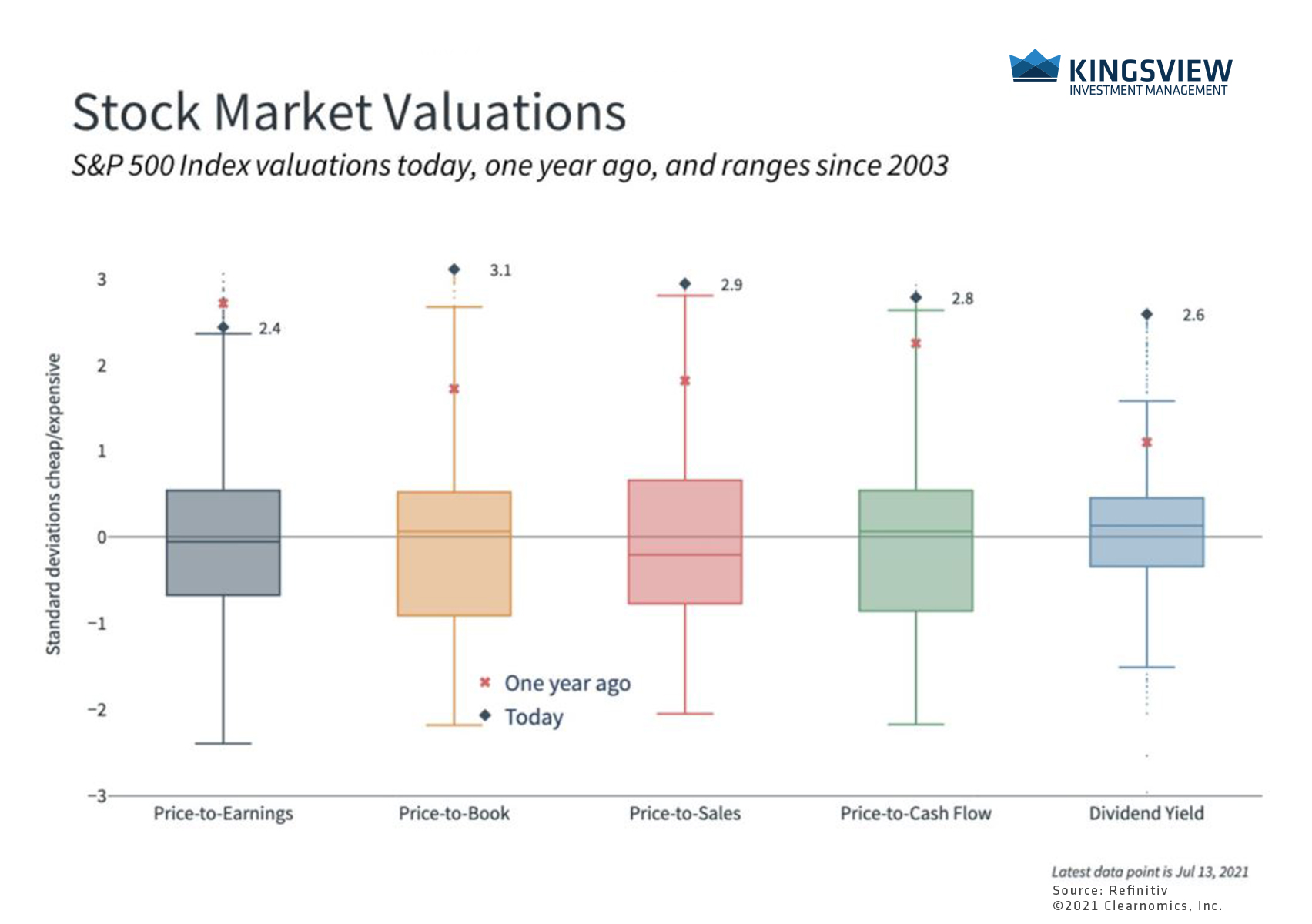

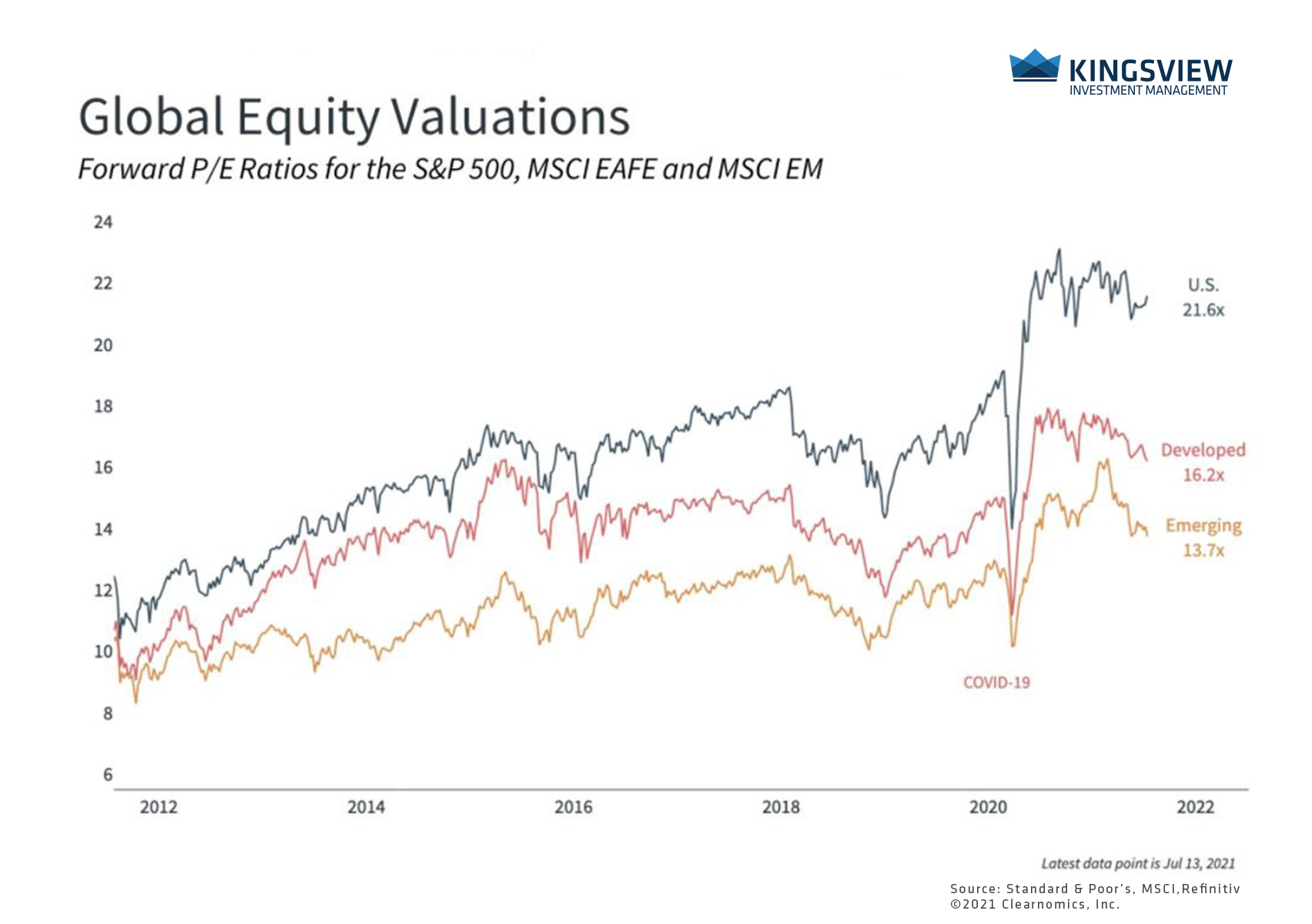

Today, various measures of value are at or near all-time highs not just for publicly traded stocks, but across a variety of asset classes. This is because the bull market has boosted prices faster than fundamentals over the past year. The closely watched price-to-earnings ratio using next-twelve-month earnings estimates is hovering around 21.6x, not far from the tech bubble peak of 24.5x. The Shiller P/E ratio, also known as the cyclically-adjusted P/E since it uses ten years of inflation-adjusted earnings, is also elevated at 38x.

This is true across measures as fundamentals improve

KEY TAKEAWAY:

- There are few valuation measures that are cheap across publicly traded stocks and other asset classes. Many measures are near historic levels going back to the early 2000’s.

This same pattern can be found across a wide variety of valuations measures, from price-to-sales to dividend yields. Across asset classes, especially public equities, there are very few areas that are “cheap” in absolute terms today.

While investors should be aware of these facts and may find it prudent to make some portfolio adjustments, there are a few reasons investors shouldn’t completely overhaul their plans. First, while valuations are helpful tools for evaluating the attractiveness of investments, they do not predict market behavior in the short run. Markets can continue to rise or fall regardless of valuations for long periods of time, especially during the earlier stages of a bull market when the underlying trends are positive.

Second, why valuations are high matters. While prices have certainly risen, valuations such as P/Es are elevated because fundamentals are still catching up. As earnings accelerate, P/E’s can moderate to more reasonable levels. On their own, P/E ratios don’t tell us whether it’s prices that will fall or earnings that will rise. In reality, the latter is already occurring as companies and consumers spend more.

Diversified portfolios can benefit from more attractive regions and asset classes

KEY TAKEAWAY:

- It’s important for investors to stay diversified in this environment since other regions and asset classes may provide more value than U.S. stocks alone.

Third, in an environment in which all asset classes are increasingly expensive and the value of cash is eroding due to inflation, staying diversified is still the best approach for long-term investors. Other asset classes including fixed income and international stocks can still help improve returns and lower portfolio volatility even if their valuations are also above average.

Where valuations go from here will be important for the direction of long run returns. However, investors should continue to stay invested and diversified as the cycle shifts from a recovery phase to an expansionary one. As portfolios benefit from the ongoing bull market, it’s also important for investors to stay invested and diversified to manage elevated valuations.

Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser. (2021)