- 2026-05-04

- Posted by: kimsite

- Categories: Insights, Volume Analysis

CHIEF TECHNICAL ANALYST, BUFF DORMEIER, CMTⓇ

Sell in May & Go Away?

Last quarter, the bulls were challenged to put up or shut up. This week, they put up on price, but volume left room for doubt

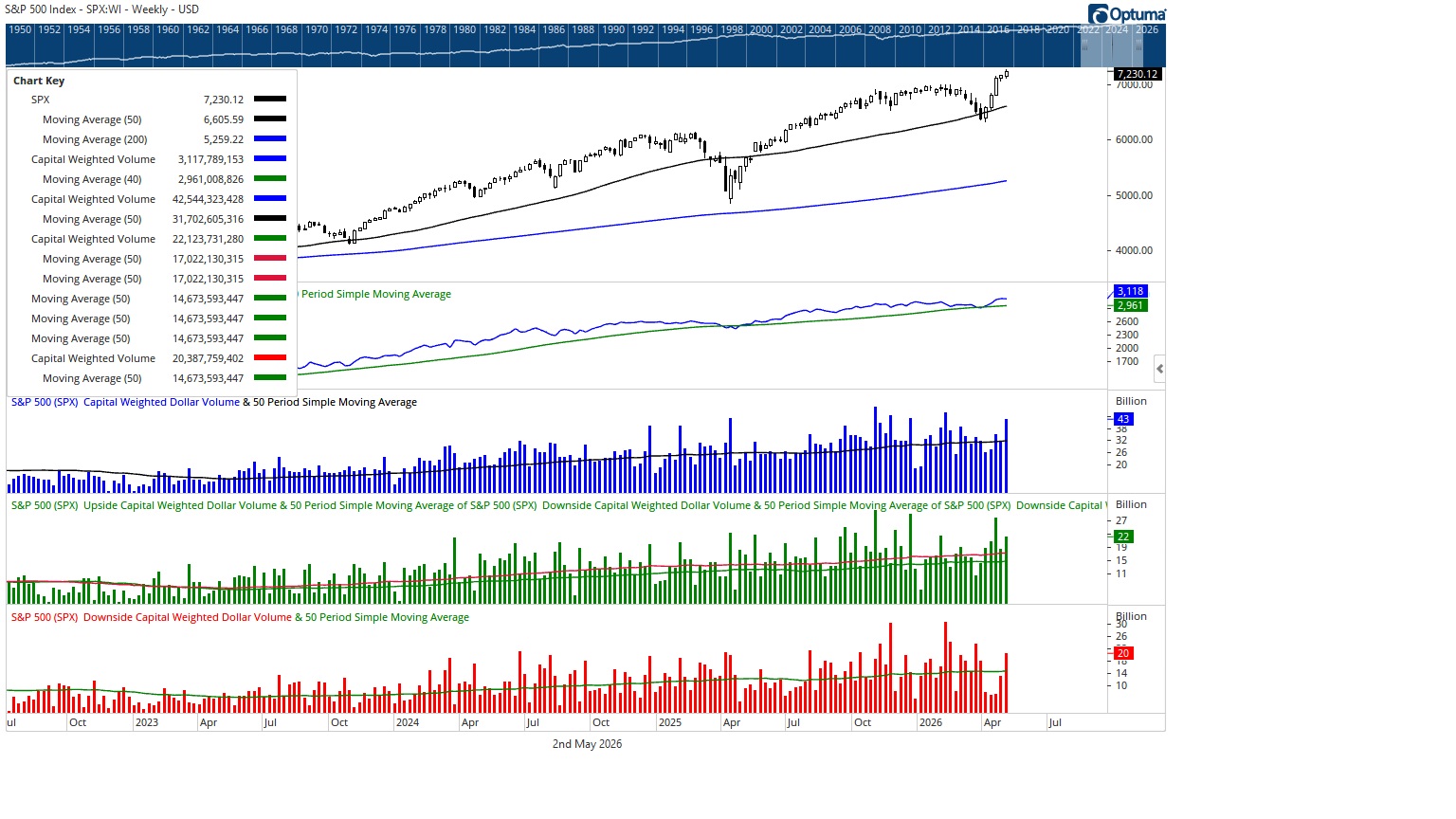

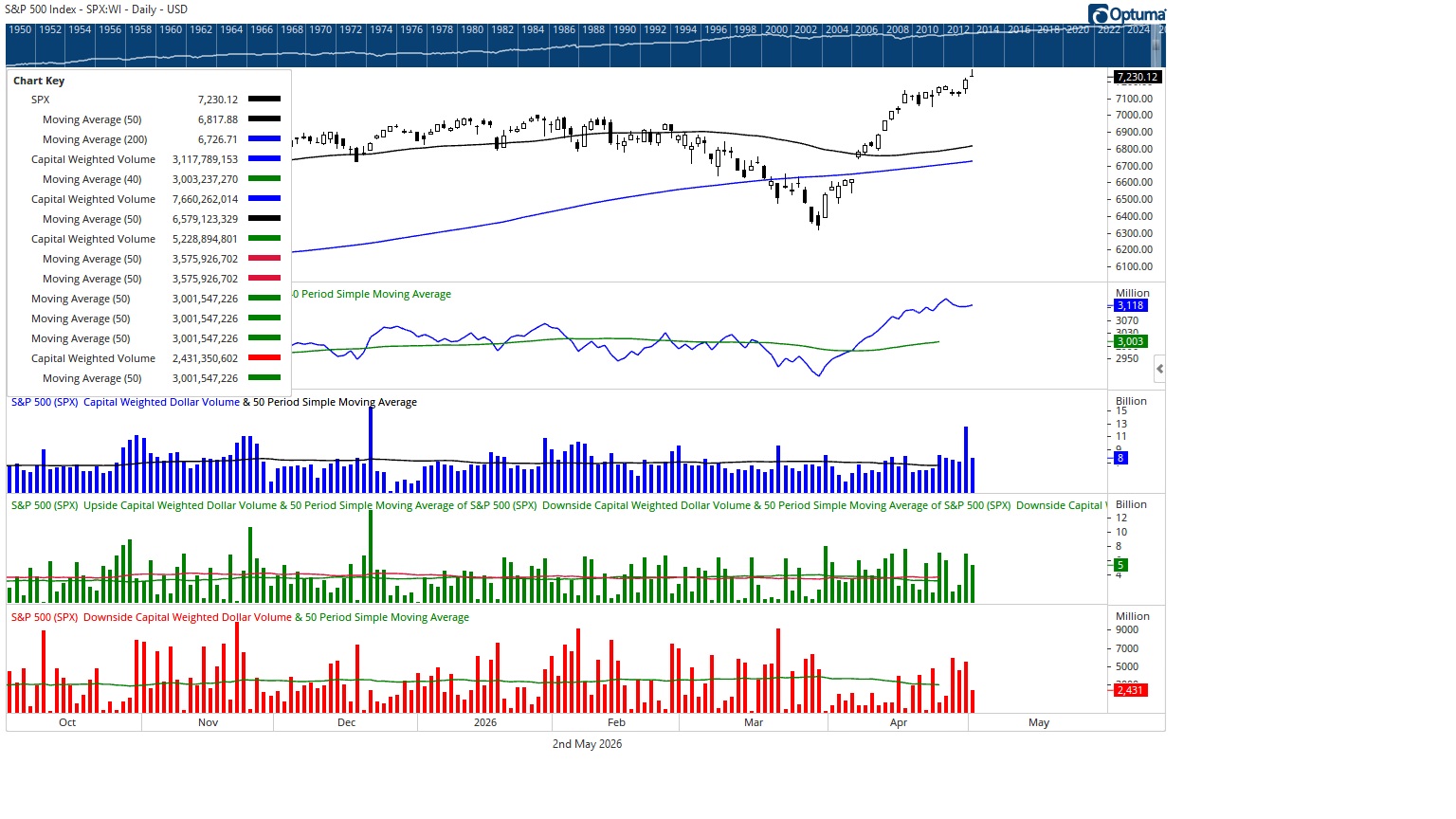

It was a data and earnings-driven week, with the market moving mostly sideways on average volume until midweek. Then on Thursday, the bulls broke loose, driving the S&P 500 to new all time highs while S&P500 capital flows doubled its average daily pace for the strongest print of 2026. Yet beneath the surface, the assault was not as decisive as price suggested, with only 55% of capital flows registering to the upside.

Friday brought another push higher as the market gapped up and advanced sharply into midsession. However, by the close, the S&P 500 had surrendered much of the advance and finished near the lows of the day, forming a gravestone doji. Readers may recall our November 3rd commentary, “Trend or Trick, Gravestone on Halloween,” when a similar S&P 500 gravestone doji marked the high and halted the bullish advance.

In Japanese candlestick analysis, the gravestone doji represents a failed rally and a potential warning that buyers lost control near the highs. The current setup is eerily similar. The key distinction is that this time volume is no longer leading price in the same bullish manner as in Q3 of 2025. The question now becomes whether something wicked comes this way once again or whether this formation proves to be a false omen.

Seasonality adds another layer to the battlefield. In the April 6th edition, we noted that April has historically been one of the stronger months of the calendar. With May here, could this gravestone doji be whispering the old market refrain, “Sell in May and go away?”

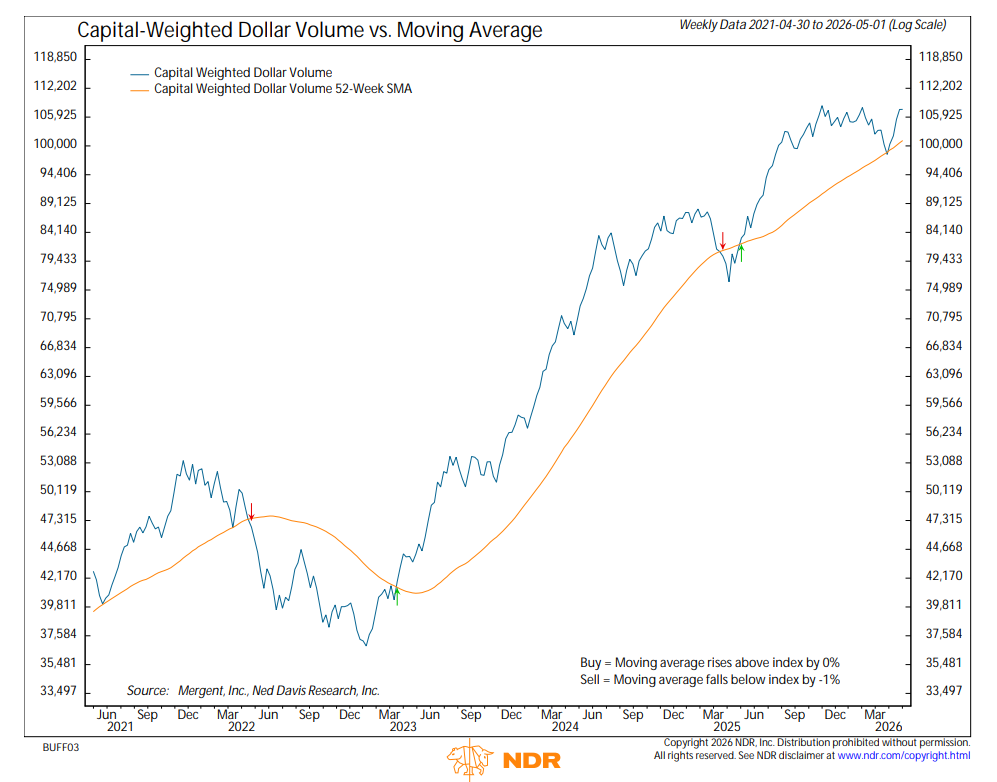

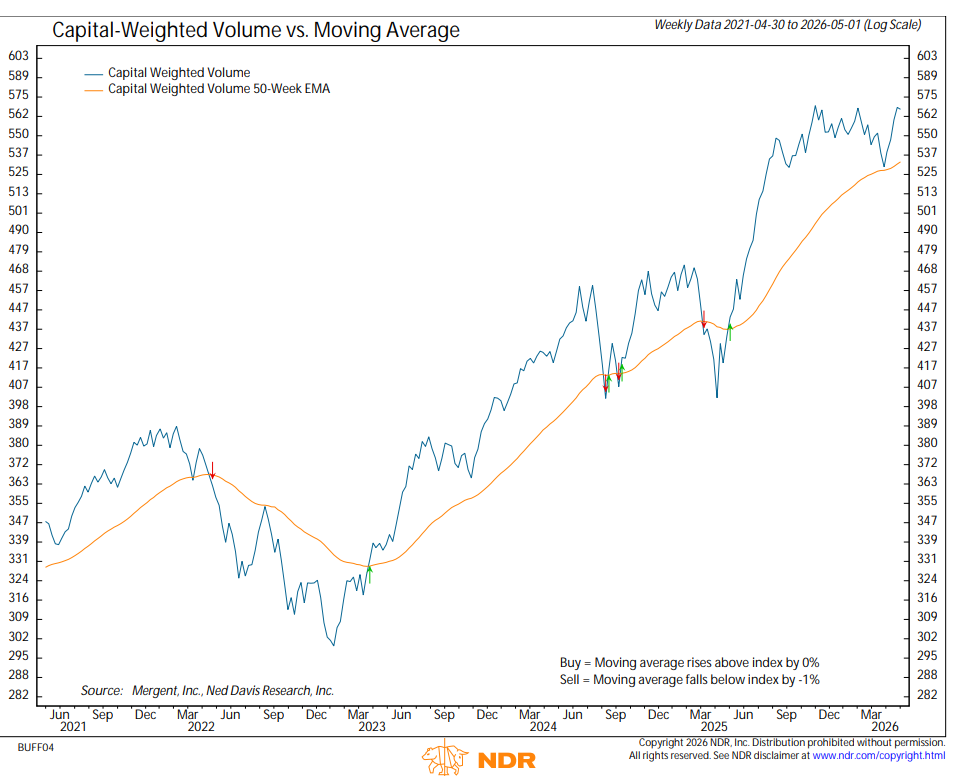

For the week, capital movements were the highest since February 9th. Despite the S&P 500 advancing nearly 1%, capital flows were mixed. Capital Weighted Dollar Volume registered 53% inflows versus 47% outflows. On the Capital Weighted Volume side, downside volume actually led upside volume 51% to 49%. Both accumulated trends of Capital Weighted Volume and Capital Weighted Dollar Volume flattened during the week and remain below their 2025 highs. Price has broken higher, but the supply lines have not confirmed the march to new heights.

Market breadth also failed to reinforce the advance. After testing the lower end of its range early in the week, the NYSE Advance Decline Line closed flat and remained inside the wide range established on April 17th. Breadth did not break down, but it also did not join the victory parade.

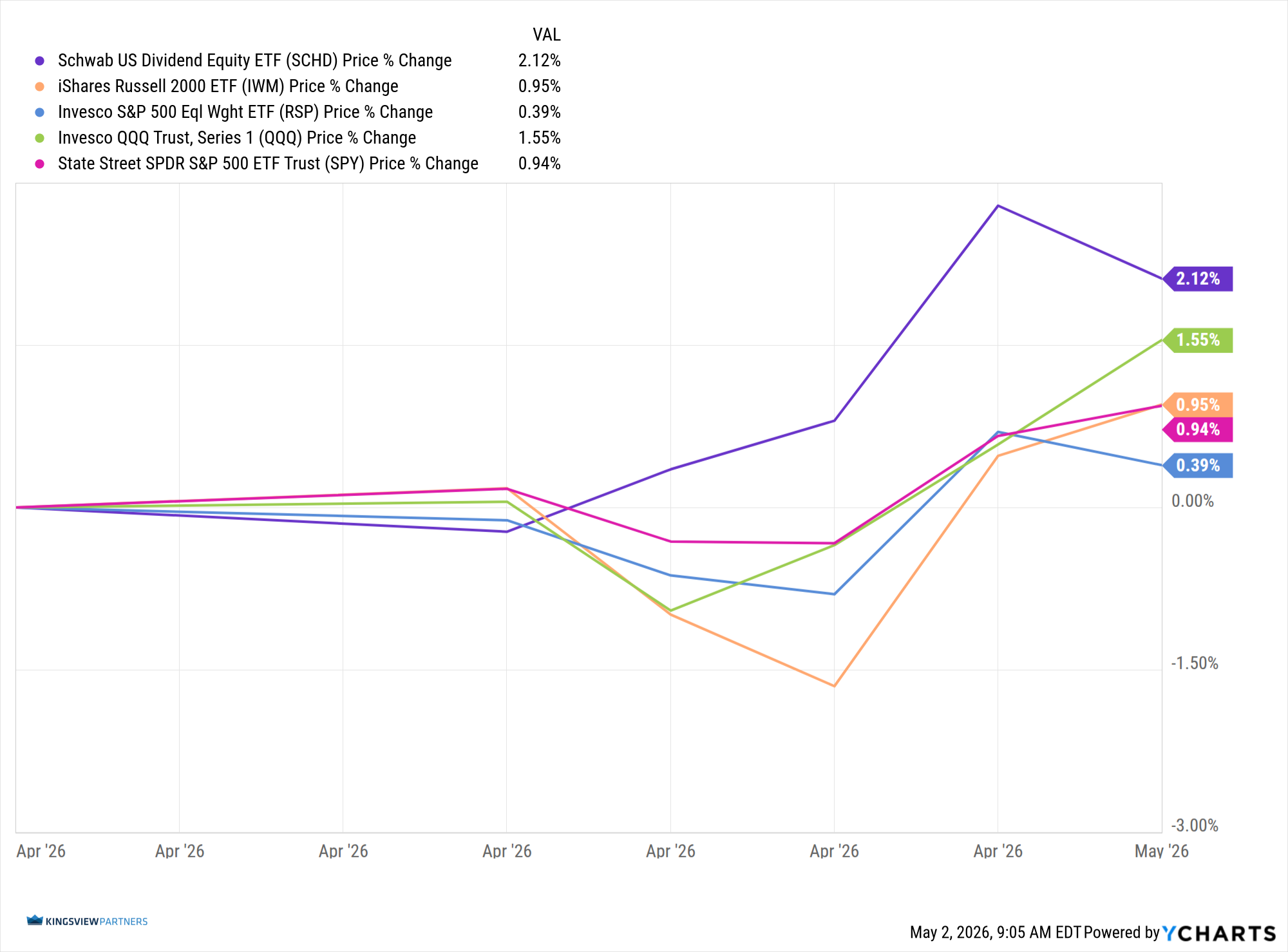

Among the field units, the brass commanders finally arrived. The Schwab U.S. Dividend Equity ETF, which had been largely uninvited to the April rally, led the week with a 2.12% gain. The generals, represented by the Invesco QQQ Trust Series 1, followed with a 1.55% advance. The troops, represented by the iShares Russell 2000 ETF, gained 0.95%. Meanwhile, the lieutenants, represented by the Invesco S&P 500 Equal Weight ETF, continued to lag with a modest 0.39% gain.

Overall, most units appear stretched from a volume perspective, with the notable exception of the brass commanders. Their late arrival may represent healthy rotation, but it also raises the possibility that leadership is shifting just as the broader advance tires.

Cross-asset action remained shaped by the ongoing Iran war backdrop. Oil, represented by NYMEX crude, briefly broke above its established trading range early in the week, but failed to hold the advance and closed back inside the range, well off the weekly highs. Still, it finished at its highest closing level since March 20th, suggesting the energy front remains active but not yet decisive.

Precious metals also showed signs of hesitation. Silver, represented by the iShares Silver Trust, closed within the wide March 20th range and formed a doji of indecision. Gold, represented by the SPDR Gold Shares ETF, closed lower near its March 13th support range, engulfed within the prior week’s range, and forming a spinning candle pattern. In military terms, the commodity scouts are oscillating, but no clear orders have been issued.

In the spirit of And Then There Were None, the advance continues, but confirmation is becoming more selective. Price has reached new ground, yet volume, breadth, and several supporting units remain less convinced. The bulls have taken the hill, but they have not yet secured the perimeter.

Risk Command

This is not an outright call to retreat, but it is a call for discipline. New highs deserve respect, but gravestone dojis, flattening volume trends, and mixed breadth deserve attention. Investors should avoid assuming that price alone confirms victory. Position sizing, diversification, and respect for key support levels remain critical. If volume and breadth rejoin the advance, the campaign can continue. If not, the old seasonal warning may gain force.

Grace and peace,

BUFF DORMEIER, CMT

Updated: 5/4/2026. Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. Investment advisory services offered through Kingsview Wealth Management, LLC (“KWM”), an SEC Registered Investment Adviser.